In brief

On 15 June 2026, the Monetary Authority of Singapore's (MAS) revised framework for Single Family Offices (SFOs) ("New SFO Regime") came into force under the Securities and Futures Act 2001. The New SFO Regime is a structure-agnostic framework aimed at harmonising the criteria for a simplified class exemption regime ("SFO Exemption") and addressing money laundering risks posed by SFOs in a risk-proportionate manner.

This article sets out key elements of the New SFO Regime, as well as the steps that new and existing SFOs need to take to operate under the New SFO Regime.

If you have any questions on how this may impact your business or operations, please feel free to reach out to us.

How does the New SFO Regime affect SFOs?

The New SFO Regime affects new and existing SFOs differently:

(a) New SFOs that commence operations from 15 June 2026 onwards - A Notice of Commencement of Business ("SFO Notification") must be filed with MAS within 14 days of commencement of operations in Singapore.

(b) Existing SFOs that are already operational before 15 June 2026 (in reliance on a licensing exemption) - An SFO Notification must be filed with MAS by 15 June 2027.

The SFO Notification is filed with MAS via: https://go.gov.sg/sfo-commencement-of-business. A system-generated acknowledgement will be issued when an SFO Notification is successfully filed.

Service providers (e.g. legal or compliance advisory firms) may file the SFO Notification on behalf of an SFO using their own Corppass account.

Prior to filing the SFO Notification, an SFO (both new and existing) must first meet the relevant requirements and conditions to qualify under the SFO Exemption ("SFO Conditions").

What are the SFO Conditions?

An SFO must satisfy the following key requirements and conditions to qualify under the SFO Exemption:

(a) Persons who can benefit from the SFO's management An SFO can only conduct fund management for, or on behalf of:

(i) Members of the same family (including family trusts and companies wholly-owned or for the sole benefit of the family)

(ii) Charitable organisations which are exclusively funded by the family

(iii) Its key employees (i.e., executive directors, chief executive officer, chief financial officer and investment professionals). Only up to 10% of the total value of the SFO's assets under management in aggregate can be attributed to key employees.

(b) Ownership of SFO: An SFO may be held via a trust, foundation or any other legal structure, so long as its funding originates exclusively from members of the same family (whether directly or indirectly), and key employees (up to 10% non-controlling stake).

(c) Incorporation in Singapore: An SFO must be a Singapore-incorporated company.

(d) Bank Account: An SFO and its fund vehicle(s) (FVs) must each maintain a bank account with a MAS-licensed bank. However, foreign-established FVs may instead maintain a bank account with a bank in a jurisdiction that complies with the anti-money laundering and countering of financing of terrorism requirements consistent with the standards set by the Financial Action Task Force.

(e) Contact person in Singapore: An SFO must, at all times, have an employee who is ordinarily resident in Singapore (i.e., primarily based in Singapore and has a Singapore residential address) designated as the SFO's designated contact person to facilitate communication between MAS and the SFO.

How is a "family member" defined under the New SFO Regime?

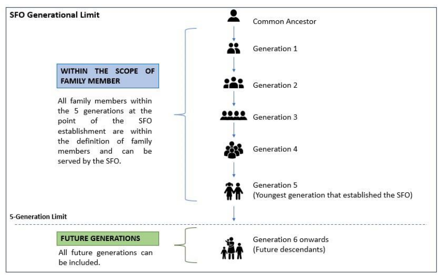

"Family member" refers to all lineal descendants of a common ancestor (living or deceased). This includes current or former spouses, adopted children, stepchildren, parents-in-law and siblings-in-law. The common ancestor must be not more than five generations removed from the youngest generation that establishes the SFO in Singapore. Please see the diagram below for an illustration.

Source: MAS' FAQs on Licensing Exemption Framework for Single Family Offices

What information must be provided under the SFO Notification?

The following information needs to be included in the SFO Notification:

(a) Full name of the SFO

(b) Unique Entity Number (UEN) of the SFO

(c) The SFO's financial year end

(d) Amount of total assets managed by the SFO at latest financial year end (SGD)

(e) Name of MAS-licensed bank that SFO has a bank account with

(f) Name of licensed bank that the SFO's fund vehicle has a bank account with

(g) Name and email address of the SFO's designated contact person/employee

(h) A declaration letter on the matters set out below, which is furnished on the SFO's letterhead and signed by (i) a family member who provided the assets to be managed, and (ii) a director of the SFO ("Declaration Letter").

Is a legal opinion required for the SFO Notification?

No, a legal opinion is not required to be submitted with the SFO Notification. That said, SFOs must ensure they can satisfy all the SFO Conditions and declare this to MAS (via the Declaration Letter) when they submit the SFO Notification.

Separately, do note that SFOs that had applied for tax incentive under Section 13O or Section 13U of the Income Tax Act, and previously furnished a legal opinion to MAS as part of their applications, will need to obtain a new legal opinion with reference to the SFO Exemption. MAS has clarified that this is necessary because there are additional exemption criteria imposed on SFOs under the New SFO Regime.

Can an SFO which does not meet the SFO Conditions apply for a licensing exemption or a capital markets services licence for fund management?

Save for exceptional reasons, MAS will generally not grant case-by-case exemptions. It is also not MAS' intention to license SFOs as they manage their own assets or assets belonging to members of the same family.

After the SFO Notification is filed, is there any other filing required?

Once an SFO is operating under the New SFO Regime, the SFO must file an annual return with MAS within four months of the end of its current financial year. The information that must be provided under each annual return largely mirrors that of the SFO Notification. MAS will not grant any extension for the lodgment of annual returns.

However, there is no need to submit an annual return in respect of the SFO's previous financial year before the SFO submits the SFO Notification.

Similar to the SFO Notification, service providers (e.g., legal or compliance advisory firms) may file the annual return on behalf of an SFO using their own Corppass account.

* * * * *

![]()

© 2026 Baker & McKenzie. Wong & Leow. All rights reserved. Baker & McKenzie. Wong & Leow is incorporated with limited liability and is a member firm of Baker & McKenzie International, a global law firm with member law firms around the world. In accordance with the common terminology used in professional service organizations, reference to a "principal" means a person who is a partner, or equivalent, in such a law firm. Similarly, reference to an "office" means an office of any such law firm. This may qualify as "Attorney Advertising" requiring notice in some jurisdictions. Prior results do not guarantee a similar outcome.